The Future of a Hydrogen Project

Earlier this year, the UAE held the Connecting Green Hydrogen MENA 2022 conference which members of the WFW Dubai structured finance and energy & projects teams attended. Green hydrogen will be a key part of the world’s transition to net zero carbon emissions, and its utilisation (through various forms) will be an important feature of the next 30 years as use of green hydrogen-related energy in the global economy increases. We believe this will be particularly prevalent in high polluting industries where electrification is either not possible or less feasible.

The hydrogen industry is in its infancy, both from a financing and development perspective. In exploring how we believe the legal framework and financial bankability structure will develop over time, we therefore draw parallels with similar power production and development areas, the most appropriate and comparable being LNG and oil and gas production.

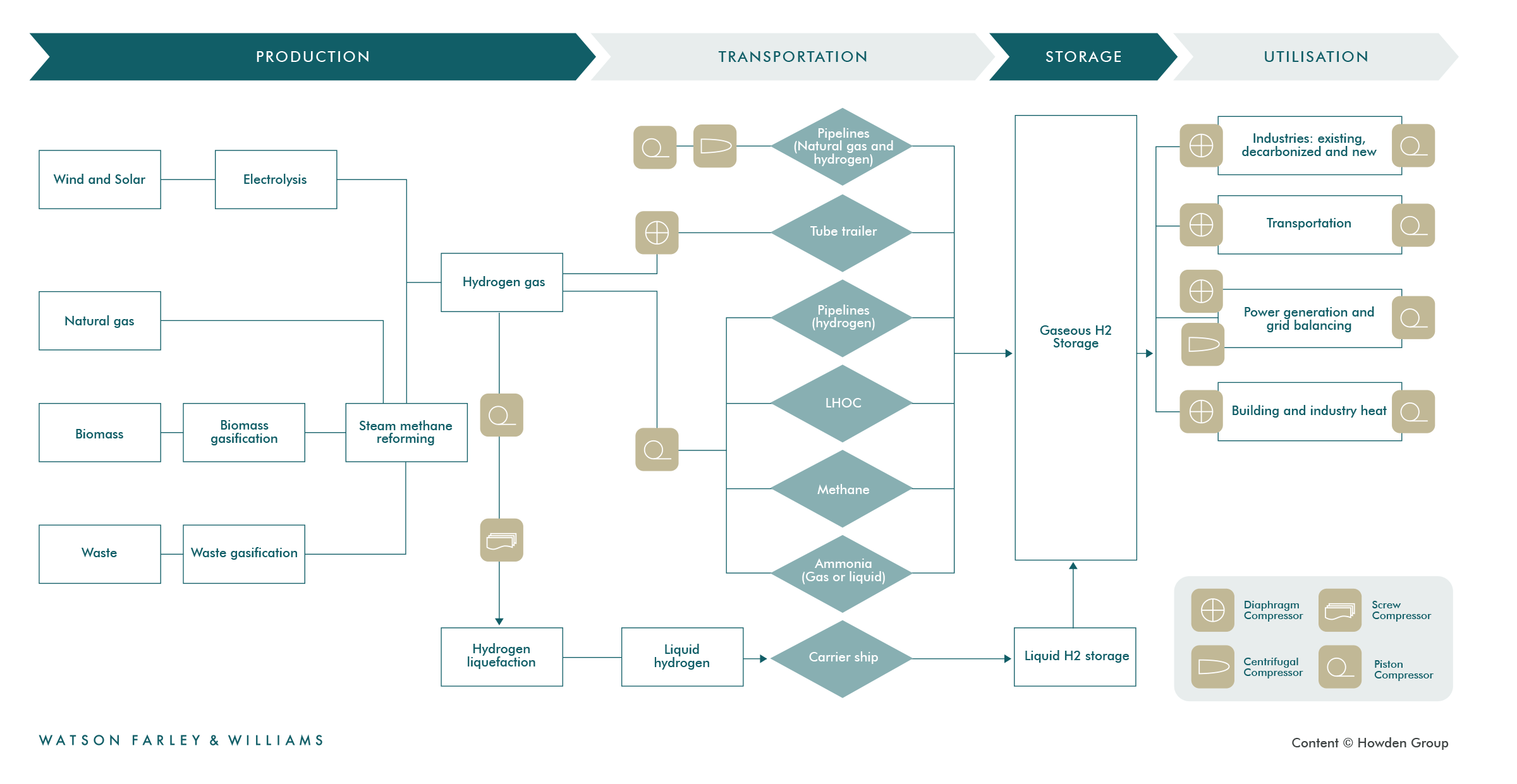

Producing green hydrogen is not a simple extraction exercise. Hydrogen production is similar to LNG production in the sense that there is an original energy source that is then transformed into hydrogen (by means of wind, natural gas, biomass or waste/waste gasification), which can then be turned into liquid hydrogen, liquid or gas ammonia, methane, or transported as a gas. One of the benefits of hydrogen is that, unlike a battery, hydrogen storage does not lose significant energy and can be converted back into electricity for utilisation (albeit at the cost of losses). Additionally, hydrogen or products from hydrogen (such as methanol or ammonia) can also be used as a feedstock in high polluting industries, such as mining, general industry, shipping, and aviation.

FINANCING CONSIDERATIONS

Some of the key takeaways from the conference were that:

- Hydrogen is still in its early stages, in terms of investor and user awareness and the actual capability of the technology and energy.

- Significant capital investments will be needed for a scalable green hydrogen project to emerge as well as a market.

- One of the main concerns arising from investors was the need for a strong sponsor driving the project to be comfortable from a bankability perspective.

- Additionally, there will need to be evidence that there is a strong market to supply hydrogen to which at present there is not. This creates a catch 22 scenario in terms of next steps for hydrogen as an area whereby sponsors and investors balance a first-mover advantage perspective against the risk of oversupply and/or a low return on investment.

However, with energy markets globally currently in turmoil and economies at present beginning to be more inward-looking than globalisation-focussed, we anticipate governments will look towards incentivising energy production such as hydrogen (through renewables and nuclear power) to develop energy independence and not rely on a foreign fossil fuel import economy. Further, green hydrogen has an inherent risk mitigant built into it by having the ability to redirect the renewable energy production to the electricity grid rather than to electrolysis, and this can assist current energy majors such as BP, Shell and Exxon (to name a few) to diversify their assets and get projects up and running despite there being no real hydrogen market at present.

There are many geopolitical factors that will impact how financing will be put in place. For example, in Europe, project financing (in most cases) will take away the ability of a developer to receive public funding. However, in regions like the Middle East, this is less of a consideration due to the intrinsic links between national champions and the state. As such, we anticipate green hydrogen projects fitting into a limited recourse project financing arrangement in the Middle East.

Please click on the thumbnail for a more detailed diagram.

PROJECT DEVELOPMENT AND COMMERCIAL RISK CONSIDERATIONS

In respect of the project development considerations, on large scale hydrogen developments we see there being a risk in proceeding with a single construction solution for the various production and construction needs. Therefore, a split construction package may be needed – this is explored further below. Additionally, there are also operational phase risks to consider once the project is producing hydrogen and has potential offtake.

Construction phase

Construction of a hydrogen plant will share many of the risk/mitigant features that arise on many other construction projects. These include for example risks of delay in completion and underperformance at completion mitigated by, among other things, liquidated damages, experienced contractors and insurance. For large scale hydrogen projects, it is likely that a multi-contracting strategy will be used because of the disparate nature of the component parts of the project. Using multiple contracts though brings in several challenges, for example, certainty of construction cost, certainty of timetable and meeting contractual completion dates, and certainty of revenues and performance at completion. Contractual interface risk is always difficult to manage during the construction phase. Creditors will expect to see a robust regime passing liability or relief up and down the contract chain, and across a multi-contract structure, as consistently as possible. However, on smaller scale green hydrogen developments, if the scale does not pose a risk on a single contractor approach, and because the renewable and electrolysis infrastructure is a common and well-developed technology, developers may seek to streamline developments in this manner with a single contractor and one stop method.

Operational phase

In respect of the operational phase of a project, sponsors will usually look to have any completion support fall away as well as to have more flexibility on ownership. In respect of a hydrogen project, given it is untested whether completion support can fall away and a project remain successful, that approach may not be possible. This will be impacted by the fee structures put in place in the O&M agreements, the nature of the supply and payment obligations under the offtake agreements and also how bankable the fuel supply agreements are, and how credit-worthy the power purchaser/fuel supplier are in practice. Further, more risks will become apparent as hydrogen projects are developed but a main operational risk foreseeable at present is the size of the actual and potential hydrogen offtake market.

A sponsor or lender will need to consider the operational and construction risks when conducting feasibility and bankability assessments of developing or financing a hydrogen project, and in particular how these risks can be offset in respect of first of their kind transactions.

CONCLUSION

This article briefly engages with particular challenges when presented with a potential project financing of a hydrogen project. There are many other risks to be considered that are common to all power projects and we have highlighted some of the contractual ones above; others would include currency conversion, repatriation of monies, the local legal regime and so on.

From the lenders’ perspective, the bankability challenges that all risks present relate to the certainty or otherwise of:

- Costs of construction and operation;

- The construction schedule and date for completion;

- The performance of the hydrogen plant at completion and beyond; and

- The revenue to be generated by it.

In the context of hydrogen projects, these are likely to be complex risks because of the use of multi-contracting strategies and the dependence of the project on the entire supply chain of the hydrogen. The key mitigants which lenders will expect to be deployed will be familiar from any project financing but will require tailoring to the specific context of the hydrogen power risk matrix: ownership and completion support, robust contractual risk allocation, experienced and credit-worthy counterparties, export credit agency cover and a strong, well-capitalised sponsor.

We wait to see how the hydrogen economy and any specific projects, and their financing arrangements, will develop over time. We will continue to follow developments in this area and share our thoughts on them in future articles.

WFW article by WFW Dubai Partners Alhassane Barry and Michael Savva,

Information Source: Read More

ENERGY | ELECTRIC POWER | NATURAL GAS | AUTOMOTIVE | CLIMATE | RENEWABLE | WIND | TRANSITION | LPG | OIL & GAS | SOLAR | ELECTRIC VEHICLES| BIOMASS | SUSTAINABILITY | OIL PRICE |COMMODITIES | ELECTRIC POWER | NUCLEAR | LNG | REFINED PRODUCTS | SHIPPING|