Alternative Fuels – Effect on Shipping Industry

WFW insight on what the future holds for shipping?

The shipping industry has a vital role in a net zero carbon future. In response to the Paris Climate Accord, the International Maritime Organisation has set ambitious goals of halving greenhouse gas (“GHG”) emissions by 2050, compared to 2008, while at the same time reducing carbon dioxide emissions intensity by 40% by 2030 and 70% by 2050.

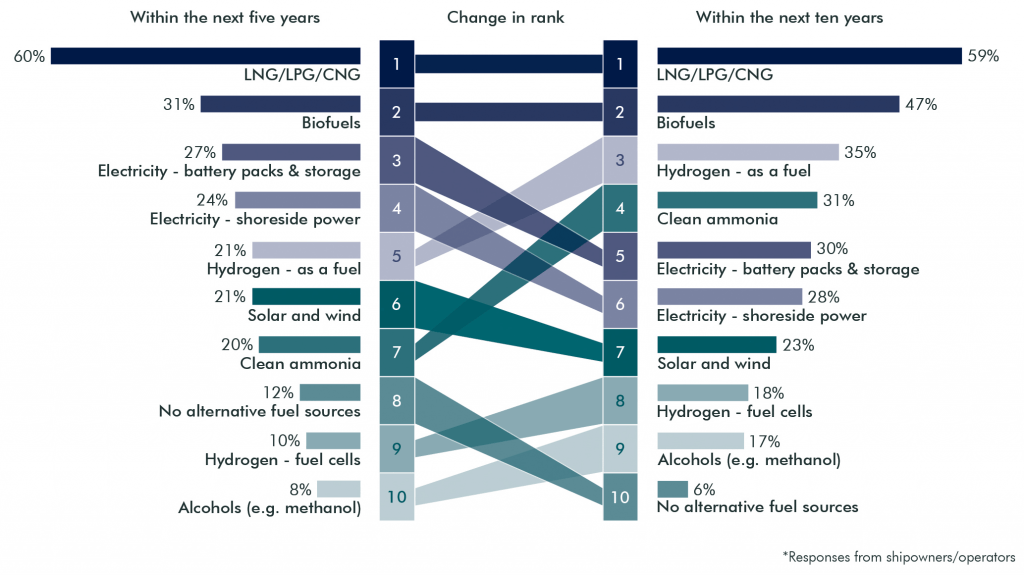

In our recent report “The Sustainability Imperative” – which drew on a series of in-depth interviews and a global survey of 545 senior industry leaders – the results showed that fewer than a third of shipping operators plan to use any alternative to traditional bunker fuel or liquefied gas such as LNG or LPG in the next five years; possibly out of caution and a desire to avoid making what might turn out to be the wrong choice in a 20 to 30-year investment. That said, the report also indicated that, as one source commented, “other alternative fuels need to come after LNG and the industry needs to keep working on finding those future carbon-neutral fuels”. It was also interesting to see from the report which of the alternative fuels are currently being considered by survey respondents as indicated in the diagram below.

Alternative fuel sources being considered for future use

The following is a brief summary of possible fuels to replace heavy fuel oil (“HFO”). It seems clear that there will be a continuing need for liquid fuels for the deep sea fleet and for long sea passages as no other way to store large quantities of energy has yet presented itself. There are a number of additional solutions focusing on battery or hybrid technology that seem better suited to the short sea fleets as these have to travel less distance between potential recharging/refuelling stations. Those technologies and how they may change the current trading patterns will be the topic of a later article. While some of these fuels (and technologies) may eventually prove to be intermediate solutions, they remain an essential part of the industry’s journey to its carbon neutral future.

Conclusion

It is clear that no one fuel currently presents a complete solution. Those listed above that currently have widespread commercial application reduce, but do not eliminate, carbon emissions from their use. Some critics even go as far as to say they pose a greater risk because of the warming effect of intentional and unintentional escapes of the fuel. Hydrogen and ammonia which appear to be cleaner alternatives for the future are not yet ready for widespread commercial implementation and that day seems some way into the future.

Evidence on climate change means that action to use an alternative fuel source is required immediately. Still in question is who should take the lead in funding research into alternative fuels and other efficiencies for shipping; in our report almost half of survey respondents took the view, which was broadly shared across financiers and operators in all regions, that it falls to governments to take the lead on this. In the absence of a clear single solution and given the range of options (none of which are particularly complementary), the industry would benefit from at least incentivisation and guidance (if not more) as to the choice to make. A swift move towards an interim ‘transition’ (or ‘transitions’) whose benefits outweigh the disadvantages, and which did not inhibit the implementation of an ultimate solution would surely be beneficial if it could be achieved

Read Full Report ..–>

By: David Handley ,Senior Associates, WFW Maritime and: Marinos Papadopoulos ,Senior Associate, WFW London

Submitted by: Will Salomone, Senior External Communications Manager