02 Nov OPEC+ production cuts support crude oil prices

Crude oil trades near the top of its current range with the lack of visibility regarding the short-term direction likely to keep the market mostly rangebound with Brent having settled into the 90’s while WTI is struggling to break above $90 per barrel. Key drivers remain the supply impact of OPEC+ production cuts and upcoming EU sanctions against Russian oil while the demand side is focusing on the timing of Covid restrictions being lifted in China and a general worry about the global economic outlook

Crude oil trades near the top of its current range with the lack of visibility regarding the short-term direction likely to keep the marketmostly rangeboundwith Brent having settled into the 90’s while WTI is struggling to break above $90 per barrel. Key market focus remains the supply impact of OPEC+ production cuts and upcoming EU sanctions against Russian oil as well as a tight product market while the demand side is torn between the prospect of a pickup in Chinese demand once Covid restrictions are lifted and worries that global economic activity will continue to weaken in the coming months.

Adding to these specific oil market developments, traders are also watching the current ebb and flow in the general level of risk appetite currently being orchestrated by movements in the dollar and US Treasury yields. With that in mind the market awaits news and guidance from today’s FOMC meeting.

The attempted bounce seen this week has been led by speculation – which was later denied – that Beijing is preparing to ease Covid rules. However, most of the gains which also benefitted industrial metals held after China’s outgoing premier Li Keqiang said China will strive for a “better” economic outcome and promote stable, healthy and sustainable development, saying China’s economy is showing signs of stabilizing, as well as “rebounding momentum” thanks to stimulus.

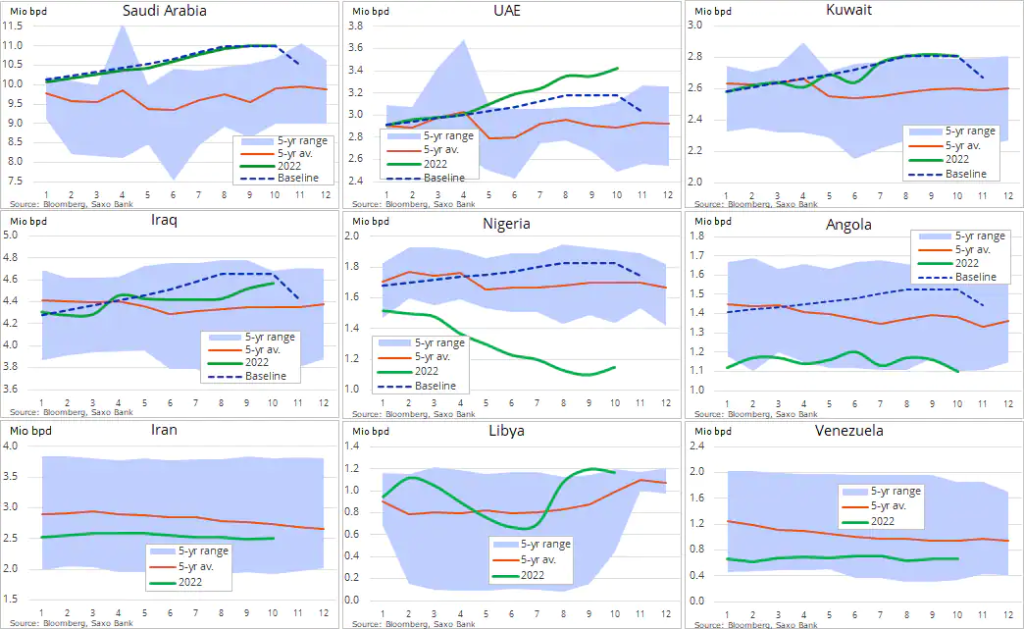

Ahead of the agreed OPEC+ production cuts this month OPEC itself, according to a Bloomberg survey, raised its output by 30,000 barrels per day in October, almost hitting 30 million barrels per day for the first time since April 2020 when Saudi Arabia temporarily hiked production just before demand collapsed as the pandemic shut down the world. While the table below only shows part of the equation the announced 2 million production cut this month will be less as several OPEC and non-OPEC+ members are struggling to reach their baseline production target. Overall, the cut is likely to be around 1.2 million barrels per day with just a handful of producers cutting, four of them shown below.

Apart from today’s FOMC announcement, the market will also be watching EIA’s weekly storage report, not least after the American Petroleum Institute last night released their report showing a counter seasonal6.5 million barrel drop in US crude stocks. In addition, the market will also be watching changes in gasoline and distillate stocks, both currently at precariously low levels and for signs of a pickup in refinery demand as seasonal maintenance ends. The level of crude and product exports will also be watched after record crude exports in the previous week helped drive total exports of crude and fuel to a record 11.4 million barrels per day.

Information Source: Read More By Ole Hansen, Head of Commodity Strategy,Saxo Bank

Energy Monitors | Electric Power | Natural Gas | Oil | Climate | Renewable | Wind | Transition | LPG | Solar | Electric | Biomass | Sustainability | Oil Price |

Sorry, the comment form is closed at this time.