Tighter than expected market conditions support crude oil

Crude oil continues its month-long rally and while the early January jump was driven by temporary supply disruptions, the rally has continued driven by signs that several countries within the OPEC+ group are struggling to raise production to the agreed levels. Adding to this a sector unloved by regulators but very much needed for years to come, and the risk of even higher prices going forward persist.

Crude oil continues its month-long rally and while the early January jump was driven by temporary worries about supply disruptions in Libya and Kazakhstan, a bigger and more worrying development has become increasingly apparent during this time. Besides the surging omicron having a much smaller negative impact on global consumption it’s the emerging sign that several countries within the OPEC+ group are struggling to raise production to the agreed levels.

For several months now we have seen overcompliance from the group as the 400,000 barrels per day of monthly increases wasn’t met, especially due to problems in Nigeria and Angola. However, in their latest production survey for December, SP Global Platts found that 14 out of the 18 members, including Russia, fell short of their targets. According to Platts the 18 members in December produced 37.72 million barrels a day, some 1.1 million barrels below their combined quota.

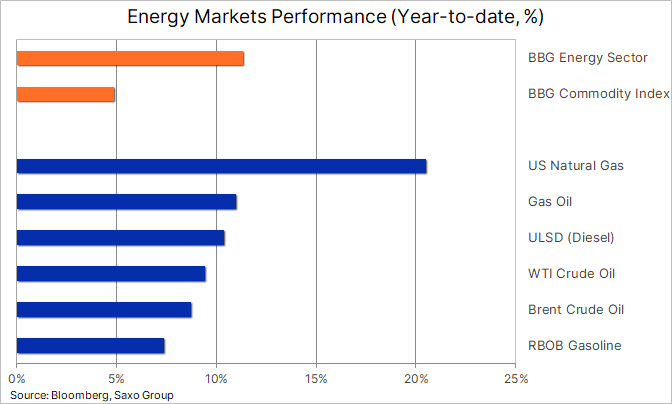

The rising gap between OPEC+ crude oil quotas and actual production has already been felt in the market with front month futures prices in both WTI and Brent having rallied stronger than deferred, thereby increasing the so-called backwardation, a curve structure that benefits long-only strategies through the positive yield when rolling (selling) expiring futures contracts at a higher price than the next month.

The US Energy information Administration was the first out of the three major forecasters, the other two being IEA and OPEC, to recognize this development. In their January Short-Term Energy Outlook (STEO), the EIA revised their Q1 global inventory outlook from a surplus to a small deficit. The report also showed that global oil stockpiles declined by a massive 3 million barrels per day in December. In addition, the EIA also forecasts that US oil production growth in 2022 would be slightly lower than previously forecast before averaging a record 12.41 million barrels a day in 2023. This in line with the latest Dallas Fed Energy survey were almost 50% of executives at 88 exploration and production firms said their focus was to grow production in 2022.

The International Energy Agency (IEA) will not publish its Monthly Oil Market Report until January 19, but with its head Fatih Birol saying “Demand dynamics are stronger than many of the market observers had thought” it is safe to assume the IEA will also lower their recent forecast for a 1Q22 surplus of 1.7 million barrels a day and 2 million barrels a day in 2Q22.

Major US shale oil producers such as Occidental Petroleum last year and more recently Pioneer Natural Resources have increasingly abandoned their forward hedging activity. Since the shale oil revolution began more around a decade ago, forward hedging has been a constant feature by many of these oil producers. During periods of ample supply, the idea made sense as forward prices traded higher than the spot market. In addition, the sector borrowed billions of dollars to pump at will, but in order to do so several were forced to hedge some of their production in order to receive their credit lines.

Surging prices since the pandemic low point, and a newfound discipline among producers cutting back their debt has given several producers the financial freedom to manage their cash flows as they see fit. But behind the decisions obviously also lies a belief that oil prices will remain at current or potentially higher levels going forward. Not least considering robust demand and dwindling spare capacity as seen through the inability by several OPEC+ members in raising production.

Despite a continued, but reduced worry about the omicron variants impact on mobility, and with demand for fuel, the outlook for crude oil remains supportive, and we maintain a long-term bullish view on the oil market as it will be facing years of likely under investment with oil majors losing their appetite for big projects, partly due to an uncertain long-term outlook for oil demand, but also increasingly due to lending restrictions being put on banks and investors owing to a focus on ESG and the green transformation.

Global oil demand is not expected to peak anytime soon and that will add further pressure on spare capacity, which is already being reduced on a monthly basis, thereby raising the risk of even higher prices. The timing of which hinges on Brent’s short-term ability to close above $85.50/b, the 61.8% retracement of the 2012 to 2020 selloff, followed up by a break above the double top at $86.75.

Source: Saxo Group

Read More By Ole Hansen, Head of Commodity Strategy, Saxo Bank

Oil and gas, press , | Energy, Climate, Renewable, Wind, Biomass, Sustainability, Oil Price, LPG, Solar, Electric,